A young person’s imagination can be a wondrous thing to behold. And, when adults play into the fantasies, it becomes even more wonderful. As a child of five years, my imagination knew few boundaries. If it existed in our backyard, I could imagine all sorts of marvelous adventures. Just give me a piece of rope and a wagon, and I was off to the never-never land of excitement. Add to this an occasional weekend trip to my Grandma Wilkens house, and the adventures took on a completely different dimension. An over-night stay at Grandma’s would usually begin on a late Friday afternoon. I was delivered to the care and feeding of my grandparents by my mother who would drop me off usually after the evening meal. After a short play time with the local in-house toy chest, it was off to a big double-bed with snuggle-down blankets. I remember the bed because it was at least three-times larger than my bed at home. The waking process was the beginning of the “Adventure” for the weekend and my growing imagination. My grandmother would awaken me with the sound of a buzzing bee. And, she would gently come beside me in the bed and pretend to “sting” me awake. The stings were more like tickles and proved the awaking process was effective. Once washed, dressed and fed, it was only a matter of a short time before Grandma and I boarded a local streetcar for an exciting trip to downtown Indianapolis. These weekend adventures took on a basic format over the years. Usually, we would arrive in the center of the city in time to do a bit of adult shopping. My Grandma was aware of my lack of interest in this part of the weekend festivities, so, she would speed through her list of things to acquire. Next would be a stop at Woolworth’s, a local “Five and Dime” Store, for a bite of lunch. We always sat at the counter, but I was usually too excited to eat more than a “bite.” Grandma would insist that I needed to finish my meal to keep up my energy for the rest of the adventures. It was what was about to take place, that was the best part of the day! We were off to one of the local movie houses for a show! Downtown Indianapolis had at least a dozen movie theaters in those days, and, quite often, there was a stage show that accompanied the matinee. Keep in mind, this was years before television. Not only did we get the latest Hollywood comedy or drama, but live performances as well. It is difficult to imagine what all that glamor and excitement did to my childhood life. It added another dimension that a whole backyard couldn’t provide. The various acts of acrobatics, juggling, dancing and singing, opened my eyes and mind to a world of entertainment that had no boundaries. And, when you throw-in “Laurel and Hardy”, the “Bowery Boys” or a “shootum-up Western,” on the same bill, it just didn’t get better than that. After leaving the theater, there was time for a quick ice cream treat, and picking up an inexpensive toy that would occupy the rest of the day at Grandma’s. My Dad would usually pick me up early on a Saturday evening and bring me back to the reality of home life minus the expanded adventure of the city. These adventures at Grandma’s continued for several years until my sister, who was two and a half years younger than I, joined the experience. She didn’t have an iota of the interest in movies or stage shows that I enjoyed, so, it didn’t take too many downtown visits before we decided that we would discontinue the excursions. Even though it has been over seventy-five years since those early days of “adventure”, they remain vivid reminders of times that were real…not imagined!

Once upon a time, taxpayers could generally deduct 50% of business-related meal and entertainment expenses. However, several exceptions allowed larger deductions in certain circumstances. The Before and After of Exceptions Under prior law, the following exceptions to the general 50% deductibility rule were available. (In some cases, as you'll see below, the exceptions have been retained under the TCJA). An employer could deduct 100% of:

In addition to the above tax write-offs, business taxpayers could, under previous law, deduct 100% of the cost of:

Effective for amounts paid or incurred after December 31, 2017, the TCJA disallows deductions for most business-related entertainment expenses, including the cost of facilities used for most of these activities. Specifically, nondeductible expenses now include:

Deductions Still Allowed Apparently, you can still deduct 50% of the cost of business-related meals with business associates. If so, the time-honored rules for proving that meals are business-related still apply. Once again, this conclusion isn't completely clear at this time. We are awaiting IRS guidance. It's clear that you can still deduct 50% of the cost of meals for you or an employee while away from home on business-related travel. In addition, a business's costs for meals and food and beverages that fall under some of the exceptions listed above are still 100% deductible (for example, when the cost is reported as taxable compensation to recipients who are employees and non-employees). Meals provided to employees subject to the DOT hours-of-service limitations are still 80% deductible. Key Point: If a hotel or other lodging establishment includes meals in its room charges or you give employees per-diem allowances that are intended to cover meals, you can use a reasonable method to determine the portion of expenditures allocable to meals and subject to the 50% deductibility rule. Ask your tax advisor about this. Tax Planning Considerations Taxpayers should assess their current expense allowance policies to determine if the unfavorable TCJA provisions warrant changes in policy — especially for entertainment expenses incurred by employees. Accounting system changes may be necessary to separately track employee entertainment expenses and employee business-related meal expenses, which may still be 50% deductible. As you can see, the treatment of meal and entertainment expenses is complicated after the TCJA. Maybe more complicated than you thought! Also, understand that what you read here is based purely on our analysis of the applicable provisions in the Internal Revenue Code. Subsequent IRS guidance could differ. Feeding Employees: Then and Now De minimis meals. Under prior law, employers could deduct 100% of the cost of food and beverages supplied to employees, if the food and beverages were tax-free to employees because they qualified as a de minimis fringe benefit. Those benefits are defined as having a value and frequency of occurrence so small as to make accounting for them unreasonable or administratively impractical. Examples include:

Employer-Operated Eating Facilities: Under prior law, employers could deduct 100% of the cost of operating a qualified eating facility for employees, such as a company cafeteria. The facility had to meet certain requirements. First, it had to be:

TCJA Change: For amounts paid or incurred from January 1, 2018 through December 31, 2025, the new law allows employers to deduct only 50% of the cost of operating a qualified eating facility for employees. After 2025, no deductions will be allowed. Employers that operate eating facilities for employees should review the costs of running their facilities and determine if the temporary 50% deduction rule and the eventual complete disallowance rule dictate a change in policy. Meals Provided for the Convenience of the Employer. Under prior law, the cost of meals furnished to an employee for the convenience of the employer could be fully deducted by the employer and treated as tax-free to the recipient. However, 100% deductibility for the employer only applied if a bevy of requirements were met. Otherwise the general 50% deductibility rule for meals applied. TCJA Change: For 2018-2025, the TCJA allows employers to deduct only 50% of the cost of meals that are provided for their convenience. After 2025, no deductions will be allowed. Then came the Tax Cuts and Jobs Act (TCJA), which dramatically shifts the playing field for expenses paid or incurred after December 31, 2017. The new law also creates some uncertainties, as this article will explain. Your tax advisor can keep you up to speed on the issues and suggest strategies to get the biggest tax-saving bang for your business meal and entertainment bucks.

Liquidity means the ability to turn an asset into cash. Having liquidity gives you the feeling of control, but liquidity provides both real control and the illusion of control. The financial reason for wanting liquidity from what are intended to be dollars left untouched until some future date, is the ability to cope with or avoid potential risk. If you have an unexpected financial emergency, being able to sell or transform an asset quickly to get dollars in your hands is real control. This is generally what is thought of when one thinks about their asset being liquid, but liquidity isn’t that simple.

Does liquidity also mean getting the money without a cost? If so, then certificates of deposit within their penalty period could be viewed as illiquid. Indeed, even money market accounts could be viewed as illiquid since federal law limits free withdrawals to not more than six per month. Typically there is a commission or fee if you sell a stock or bond – does this mean stocks and bonds are illiquid? What is the time limit on liquidity? We use words like immediate or instant liquidity, but unless the money is in our mattress or wall safe we can’t get it this very second. You typically can’t get the money for two days or more when you sell securities; is this liquid? A check is called a demand deposit, but the bank can stop access to those funds for a week by saying they have concerns over “doubtful collectability”. And if a week delay is viewed as liquid, why wouldn’t the two to four weeks it usually takes to get the check from cashing in an annuity also be liquid? And then there is the illusion of liquidity. Typically a bank will let you cash in that CD or make that seventh withdrawal from the money market account this month, but they don’t have to. A bond sale settles in two days, unless you were trying to sell many of the mortgage-backed bonds in 2008 for which there were no buyers. And, an extreme case, there was zero investment liquidity in the days following 9 -11. Although that was extreme, governmental authorities in some countries believe that some exchange traded funds (ETFs) could become illiquid during a market panic. The financial markets, banks, and even governments all operate on the illusion of liquidity believing there will always be buyers, enough people paying their debts and a government that will be able to ultimately bailout any crisis, but this is only true if people still believe the illusion. The illusion of control imagines that you will exercise that liquidity well. In the stock market the mirage is that the investor will sell out of the market just as it begins its fall – or will use the liquidity to keep moving from liquid choice to liquid choice to maximize returns. The reality is that doesn’t happen. Indeed, as Investment Company Institute data shows time after time, the liquidity is used to sell at the bottom of markets and often to leap out of rising markets. The concept of liquidity is not as clear cut as it first appears. If liquidity is defined as not having a cost then many annuities would be excluded, but so would any ETF, stock or bond where a commission or transaction fee is involved in the sale. If liquidity is defined as having instant access to the funds then every investment is ruled out as well as many bank products. What this all means is you need to ask yourself how you define liquidity and what it means to you.  Let’s start with the definition of actuarial assumptions from Investopedia, “An actuarial assumption is an estimate of an uncertain variable input into a financial model, normally for the purposes of calculating premiums or benefits. For example, a common actuarial assumption relates to a person’s lifespan, given their age, gender, health condition and other factors.” I have worked with actuaries for many years in my career. First, as president of life insurance companies when we deliberated over benefits, premium, payouts etc. The actuary was the sound voice of reason that kept us in a profitable mode. I also worked with actuaries when contracted to develop products for insurance carriers. Again, in most cases, the numbers don’t lie - that’s why we need the actuaries. So, why is it that we as human beings tend to ignore the actuarial tables when we look at our life expectancy and calculate how long our retirement funds will last? Maybe it’s because we have anecdotal evidence of premature deaths of people we have known. I have also witnessed the early deaths, but the actuarial tables show the big picture. And, chances are you are going to live longer than you might think. So, I ask you... how lucky do you feel? Let’s go to Wikipedia and look at the definition of longevity risk, “A longevity risk is any potential risk attached to the increasing life expectancy of pensioners and policyholders, which can eventually result in higher pay-out ratios than expected for many pension funds and insurance companies.” They go on, “One important risk to individuals who are spending down their savings is that they will live longer than expected and thus exhaust their savings dying in poverty or burdening relatives. This is also referred to as “outliving one’s savings” or “outliving one’s assets.” So, what does this mean? Let’s explore… First off, we all feel good about Social Security being there (at least for baby boomers) and can count on that as one source of income. Some of us are also lucky enough to have a pension. And, in most cases, that payout won’t be in danger (unless the institution is in serious financial distress). But what about the rest of your money? What about the essential income needs: housing, medical, taxes, insurance, food, etc? Is there enough cash flow? We then look at discretionary needs... vacations, gifts, new cars or whatever. How about that source of funds? Is it in good shape? Let’s look at few factors and a solution to help you sleep better at night. Okay, pull out your driver’s license and look at your date of birth. Are you at the age where you should be shouldering high levels of risk in your portfolio? Only you can answer that… but the answer is probably no. If you are withdrawing funds in this low interest environment, this could affect how long the funds will last unless you reduce withdrawal amounts. What about your money in equities? If you are like me, you’ve been enjoying the ride. But, will there be a day when the markets will decline? I don’t think I even have to wait for your answer. If that becomes the case, then your portfolio could become very damaged and the amount of your income would have to be reduced or curtailed for a while. Is there an answer? Yes… There are annuities available which will provide you with an income for life... regardless of interest rates or market turmoil. These annuities allow you to participate in the potential of growth while taking distributions. Many also provide access to funds, on top of your distributions, to be used in the case of emergencies or opportunities. And finally, you are guaranteed to never lose a penny of principal or previous gains even in the case of a market turndown. So, there you have it. The actuaries say that the risk is there. The result can be painful, but there’s an answer to this risk, and it will allow you to sleep like a baby. All you have to do is inquire and check it out. Want to know how this can be personalized to your portfolio? Contact me and I’ll give you some safe money solutions.

Over twelve million American men and women experienced service during World War II. Of that total, only several hundred thousand are still living today. They have been called the “Greatest Generation” because of their willingness to make the supreme sacrifice for their country and fellow men and women. It is to their honor we dedicate this story.

Reford Young was just twenty-one when he was drafted into the U.S. Army in 1942. A native of Pike County, Kentucky, he began his service at a basic training camp in Tennessee. Reford continued his orientation in desert training in Arizona and spent time at a base in Wichita, Kansas before disembarking for Europe from Fort Dix in New Jersey. He sailed aboard the Queen Mary to England. Upon landing, he spent a week adjusting to climate and being outfitted for combat. Reford was a part of General George Patton’s Third Army – specifically Company C 317th First Platoon. He was designated a rifleman and photographer. Because of a special request by his mother, Reford’s twin brother, Raymond, was assigned to the same outfit as his brother. Raymond had been wounded early in the fighting, thus the brothers saw limited service time together although they did see action almost immediately upon arriving in France. The Company arrived at Omaha Beach in Normandy and were under fire within a few days at Argouten, France – a hilly part of the country still held by German forces. Being new to fighting, Reford would rise up to see what enemy was near only to be shouted out by his brother, “Keep your head down!” It was ironic that Raymond was the one who was wounded and Reford went unscathed through all the action. Reford reached the rank of Buck Sergeant during this time in the service, but refused on numerous occasions to take a leadership role in his company. It was his feeling the majority of men in the command didn’t care to take orders, and he didn’t want to give them. He was content in remaining a member in the ranks – a foot soldier who wanted to complete the assignments given him, and do them as well as he could. Toward the end of 1944, the war had reached a stalemate. The Allied forces were perched on the border of Germany just waiting for the weather to break so that a successful attack could be mounted. There had been talk about the Christmas Holiday and maybe taking some time off from the front lines. That all changed on December 16th, 1944, because Hitler had other plans in mind. He would launch one more major offensive through the Ardennes Forest to divide the Allies and to secure a port cutting off their supplies. This battle was to be called the “The Bulge” and brought the siege of Bastogne to the headlines of newspapers throughout the free world. As history tells us, Hitler’s December offensive was initially successful. If it weren’t for the fortitude of a meager defensive group of the 101st Airborne in Bastogne under General Anthony McAuliffe, who refused to give ground, and a tactical chance taken by Patton’s Third Army, the outcome might have been quite different. Reford Young remembers the bone-chilling cold of foxholes and marching in mud and snow for miles to relieve the men fighting in the holding action in Bastogne. Even with their effort, the success of the operation depended upon the Army Air Corps to bomb an enemy that was dedicated to one last, desperate operation. Reford remembers an icy, snowy day in December when the skies cleared and for the first time in days, he could see the bombers and fighters overhead seeking targets that would clear the way for the Allies to break out of “the Bulge.” He was deep in his foxhole, but he couldn’t help feeling a joyful relief even though he was bitterly cold. It was the beginning of the end for the war in Europe. Hitler had spent his last effort. General Patton is quoted as saying, “The war is almost over. The God of battles always stands on the side of right when the judgment comes.” For Reford Young and his fellow soldiers, there was still plenty of war to be won. They fought their way through Germany and doubled back to end up in Austria where he ended his active war service. To his credit, Young ended up with four battle stars and numerous medals to exhibit. He was discharged from the Army in October of 1945, having sailed back to the United States aboard a luxury German ship. Today, Reford divides his time between Florida and Franklin, Indiana, where he can still be found on a local golf course tying to shoot his age which is ninety-six. We wouldn’t bet that he doesn’t do it! The Battle for Bastogne was just one example of the fortitude and desires of the men and women who are a part of the “Greatest Generation.” And, even though their numbers are reduced, the American Spirit they represent lives on in their heritage. God bless them each and every one. This article was written by: Norm Wilkens A nationally recognized speaker and writer, Norman Wilkens has traveled to forty-seven of the fifty states speaking on topics of marketing, advertising and public relations.  Equifax, one of the nation’s three major credit reporting agencies, recently reported a massive data breach. Are you among the 143 million U.S. consumers whose personal information was hacked? Here’s how to find out — and how to help protect yourself against future breaches.

What Went Wrong? On July 29, Equifax discovered that, starting in mid-May, criminals had exploited a vulnerability in a website application. Although management took immediate action to stop the attack, hackers had already gained unauthorized access to millions of consumers’ names, Social Security numbers, birth dates and addresses, along with thousands of credit card numbers and credit dispute documents that contained sensitive personal information. The attack affected individuals in the United States, Canada and the United Kingdom. Equifax immediately launched a forensic investigation and began working with law enforcement officials to discover the source and scope of the breach. Equifax has also responded by offering a free year of identity theft protection and credit file monitoring to all U.S. consumers. Has Your Personal Data Been Breached? Go to Equifax’s website and click on the “Potential Impact” tab to find out if your personal information has been compromised. The website also allows you to sign up for free data protection and credit monitoring services — regardless of whether you were affected by this particular incident. Important note: The link requires you to enter personal information. So, access it using only a secure computer and an encrypted network connection. After you request to enroll in the free service, the website will provide you with an enrollment date. Write down the date and come back to the site and click “Enroll” on that date. You have until November 21, 2017, to enroll for the free services. In addition to the website, Equifax plans to send direct mail notices to consumers whose credit card numbers or dispute documents were breached. “This is clearly a disappointing event for our company, and one that strikes at the heart of who we are and what we do. I apologize to consumers and our business customers for the concern and frustration this causes,” said Chairman and Chief Executive Officer, Richard F. Smith, in a recent statement. He added, “I’ve told our entire team that our goal can’t be simply to fix the problem and move on. Confronting cybersecurity risks is a daily fight. While we’ve made significant investments in data security, we recognize we must do more. And we will.” What Should You Do If a Breach Occurs? If you suspect a data breach, help protect your identity from thieves and minimize losses by taking these steps: Call the relevant companies if you suspect that a breach has occurred. Ask for the fraud department and explain the incident. Then change log-ins, passwords and PINs to minimize your losses. Consider freezing your credit. A credit freeze makes it harder for someone to open a new account in your name. Keep in mind that a credit freeze won’t prevent a thief from making charges to your existing accounts, however. Alternatively, consider placing a fraud alert to warn creditors that you may be a victim of ID theft. Fraud alerts are free from all three major credit reporting agencies and last for 90 days. After the 90-day window, you can renew a fraud alert, if necessary. Obtain free annual credit reports from Equifax, Experian and TransUnion. Identity theft usually results in accounts or activity that you won’t recognize. Ongoing Protection ID theft often happens long after your personal information has been stolen, so don’t allow yourself to be lulled into a false sense of security after your initial response. Ongoing credit monitoring is essential. Proactive consumers continue to watch credit card and bank accounts closely for unusual activity. They also file their taxes as early as possible — before a scammer can. If your personal data was exposed in the Equifax attack or it’s affected by another breach, contact your financial and legal advisors to guide you through the recovery process. This article was written by: The TMA Small Business Accounting, P.C. Their staff has been delivering professional services to small businesses in Central Indiana for over 20 years. Having worked with hundreds of small business clients, we have significant expertise with a wide variety of service businesses in Indiana. We have especially strong experience and expertise in working with businesses in the healthcare (medical, dental, etc.) and foodservice (restaurants, caterers, etc.) industries.

To combat fraud, European credit card issuers have opted for a two-stage security process. In addition to sticking a microchip in the card that is read when it is scanned, the cardholder also needs to have a PIN. He or she enters it when the transaction takes place. If that card is lost or stolen, the new possessor is likely out of luck without that PIN. It’s anyone’s guess as to why the Americans haven’t adopted this measure, since they just spent billions of dollars to issue new cards nationwide that carried the chip. Couldn’t they have added the PIN feature at the same time? Debit cards use them, so why not credit cards? Unless we all move to Europe, though, we’ll have to make do with the cards currently in our wallets. They’re getting safer year by year, but trouble seems to lurk around every corner where billions of financial transactions are concerned. If you’re buying online with a credit card, look for an “S” to be tacked onto the “HTTP” in the web address line. This stands for “secure,” and indicates that the merchant is scrambling communications between its website and your browser. That should keep the bad guys at bay. (HTTP, btw, means Hyper Text Transfer Protocol, which is the protocol over which data is sent). Most merchants these days also will ask for your CSC – card security code. This is a three-digit numbers group that is separate from your account number. Thanks to these transactions taking place at the speed of light, the merchant is transmitting your data to the card issuer and instantaneously halts the purchase should those numbers not match. Of course, anyone who holds your card and isn’t blind also knows that CSC (thus, the PIN is to my way of thinking a better idea). Now, if you’re at a restaurant or department store and use your card, you’re going to get a receipt to sign. Bank of America advises that if you see any blank lines on that receipt, draw a line through it to make sure no one can come in after you and pencil in some fresh numbers. If you have a choice between a credit and debit transaction with the same bank card, experts say you should choose credit. There are stringer fraud protections with credit cards. And if something bad does happen, a credit card liability is capped at $50. With a debit card it’s $500, or in some cases more. Plus, bear in mind that your debit card is linked to your bank account. Not so with a credit card. Have a merry, safe shopping, holiday season.

In evaluating the do’s and don’ts of estate planning, business succession, assistance with aging parents and general family matters, one commonly overlooked and extremely valuable tool is the General Durable Power of Attorney form. Most states have enacted and adopted statutory legislation that governs what may be included in a General Durable Power of Attorney. For example, the State of Indiana provides an exhaustive listing of what acts may be undertaken and these acts may include: selling property (real and personal), making investments and making healthcare decisions. The General Durable Power of Attorney is often chosen as a way to plan for those times when you are incapacitated. Consequently, having a General Durable Power of Attorney with a specialized agent allows your affairs to be handled easily and inexpensively. Prior to when the General Durable Power of Attorney was created, the only way to handle the affairs of an incapacitated person was to appoint a guardian; a process that frequently involves complex and costly court proceedings, as well as the often humiliating determination that the person was wholly incapable and in need of protection. Additionally, the Court proceedings would be of public record; therefore, allowing the world to know of this unfortunate time in a loved one’s life. The most important part of creating a General Durable Power of Attorney is choosing an agent. The agent is the person you select to carry out the duties you have outlined in the General Durable Power of Attorney. The agent should be someone you trust to carry out your wishes, someone who will not take advantage of you when you are incapacitated, and someone who is willing to serve as your agent. The agent is usually a family member or a friend; however, you may choose anyone. Once you have signed a General Durable Power of Attorney, you should inform your physician, your family, your banker, your insurance agent and your financial/tax advisor. You should also have multiple copies in case of your subsequent incapacitation. It is best to store such a valuable document in a personal safe or a safe-deposit box at your local bank branch. In addition to the above, it is extremely important to note that if you change your mind after creating the document you may amend, modify and/or revoke said General Durable Power of Attorney at any time.

It happens almost every Spring. There’s something in the rarified air that whispers to me that it’s time to dust off the clubs and head out to a local golf course to test my limited skills in “the game.”

It has been my great pleasure, since my days in high school, to meet the challenges of the links of golf. Few times, if ever, have I achieved even a small degree of excellence in approaching the eighteen holes that comprise the “game.”For no more reason than wanting to beat myself up, I have returned throughout the years to test my clubs against the “shank”, “slice”, “missed putt” and “flubbed drive” ending in the drink even when the water was clearly not in my target area. The “Game of Golf” to me was, and continues to be, a humbling experience. It has proven, more times than I could possibly count, that even though I might talk a decent game, I could not begin to achieve even a reasonable facsimile to back up the rhetoric. The “game” has shown that I can exaggerate with the best of them when called upon to do so! I always seemed to be at my best playing “customer golf” even when I wasn’t trying. There was a time, when I was much younger, when less than one hundred strokes for eighteen holes, was achievable. In fact, my early range was relatively comfortable in the nineties. Once, I shot an eighty-six at a country club in Anderson, Indiana. If I had known that was to be the “high mark” in terms of a “low score”, I probably would have bought drinks for everyone in the club house. However, I was too young to realize that my future fame in the game had been achieved and it was going to be down-hill from that juncture on. There were always the one or two shots on the course that forced me back for another stab at futility. I remember vividly playing in a tournament at the Elks Club in Indianapolis where my foursome started on the fifteenth hole. We turned the clubhouse corner, and I was one over par for four holes. One of the tournament directors took a look at our score card and pulled me aside to question my sizeable handicap. He obviously thought I was sandbagging. Another member of our group laughed and said, “Just wait! He’ll blow it very soon!” He was correct, on the very next hole, I shot a miserable “eight.” For the round, I barely broke a hundred. Even so, for just a few holes, visions of “Snead”, “Palmer” and “Chi Chi” danced through my limited vision. As I was saying, there always seemed to be a couple of shots that would be memorable enough that they stood out from the miserable clutter to blot out the game as a whole. I still remember those special times with reverence, hope, and longing. Even though, I haven’t touch my clubs for almost four years, I still feel a twinge of excitement when I pass the closet where the “sticks” lie in- waiting collecting dust. Today, I have come to the realization that my true golf calling is helping to conduct tournaments for charity; keeping score and selling mulligans; minding the “hole-in-one contests” and watching others trying to lower their scores. FORE! This article was written by: Norm Wilkens A nationally recognized speaker and writer, Norman Wilkens has traveled to forty-seven of the fifty states speaking on topics of marketing, advertising and public relations.  It’s already starting to feel like summer in many parts of the country. But the forecast for Washington remains unclear as officials continue to discuss various tax-related issues.

No matter what happens in Washington, don’t get stuck in a holding pattern yourself. Give some attention to business and personal tax planning this summer. Here are 10 ideas that combine tax planning with summertime fun. 1. Entertain top business clients. You may be eligible to write off 50% of the cost of business meals and entertainment if you entertain clients before or after a substantial business discussion. For instance, after you hammer out a business deal, you might treat a client to a round of golf and then dinner and drinks. The 50% limit applies to all the qualified expenses, including the amounts you pay for the client, yourself and your significant others. 2. Throw a company picnic. You can generally deduct the cost of a picnic, barbecue or similar get-together. Not only will such an event provide your workers an opportunity to relax and socialize, but the 50% limit on meals and entertainment expense deductions also won’t apply. There is one caveat: The benefit must be primarily for your employees, who are not “highly compensated” under tax law. Otherwise, expenses are deductible under the regular business entertainment rules. 3. Donate household items to charity. Are you planning to clean out the garage, attic or basement this summer? If so, you’ll probably find household goods — such as clothing and furniture — that you don’t want or need anymore. Consider donating these items to charity. Assuming they’re still in good condition, you may take a charitable deduction on your 2017 personal tax return based on the current fair market value of any donated items. Use an online guide or consult your tax professional for valuations. 4. Send the kids to day camp. Parents who need to work may decide to send young children to summer day camp while school is out. Assuming certain requirements are met, the cost may qualify for a dependent care credit. Generally, the maximum credit is $600 for one child and $1,200 for two or more kids. Note that specialty day camps for athletics or the arts qualify for this break, but overnight camp doesn’t qualify. (Remember, tax credits lower your tax liability dollar for dollar, unlike deductions, which lower the amount of income that’s taxed.) 5. Buy an RV or boat. If you take out a loan to purchase a recreational vehicle (RV) or boat for personal use this summer, the vehicle or vessel may qualify as a second home for federal income tax purposes. In other words, you may be eligible to write off the interest on the loan as mortgage interest on your personal tax return. The IRS says that any dwelling place qualifies as a second home if it has sleeping space, a kitchen and toilet facilities. Therefore, the interest paid to buy an RV or boat that meets these requirements is tax-deductible under the mortgage interest rules. This deduction is available for interest paid on a combined total of up to $1 million of mortgage debt used to acquire, build or improve a principal residence and a second residence. Interest on additional home equity debt of up to $100,000 may also be deductible. 6. Minimize vacation home use. Federal tax law allows you to deduct expenses related to renting out a vacation home to offset the rental income you receive. With summer already underway, you’ve probably worked out a rental schedule for your vacation home, but remember that you can’t deduct a loss if your personal use of the home exceeds the greater of 14 days or 10% of the time the home is rented out. If you expect to experience a loss, watch your personal use to ensure you remain below the 14-day or 10% limit. Other rules, however, might still limit your loss deduction. 7. Rent out your primary residence. Do you live in an area where a summertime event — such as a major golf tournament, arts festival or marathon — will be held? If you rent out your home for no more than two weeks during the year, you don’t have to comply with the usual tax rules. In other words, you don’t have to report the rental income — it’s completely tax-free — but you can’t deduct rental-based expenses either. 8. Take advantage of business travel. Suppose you’re required to go on a business trip this summer. You can write off much of your travel expenses as long as the trip’s primary purpose is business-related — even if you indulge in some vacationing. For instance, if you spend the business week in meetings and the weekend sightseeing, the entire cost of your airfare plus business-related meals, lodging and local transportation is deductible within the usual tax law limits. Just don’t deduct any personal expenses you incur. 9. Support a recent graduate. If your child just graduated from college, this is probably the last year you can claim a dependency exemption for him or her. However, you must provide more than half of the child’s annual support to qualify for the $4,050 exemption. To clear the half-support threshold, consider giving the graduate a generous graduation gift, such as a car to be used on the first job. Doing so will provide your child with a practical gift, as well as possibly helping you clear the support threshold required to claim a dependency exemption. Unfortunately, dependency exemptions may be reduced for high-income taxpayers. Consult a tax professional about this tax issue before purchasing a major graduation gift. It could impact the amount you’re willing to spend. 10. “Go fishing” for deductions. The IRS won’t allow you to claim deductions for an “entertainment facility,” such as a boat or hunting lodge. But you can still write off qualified out-of-pocket entertainment expenses, subject to the 50% limit. For example, if you take a client out on your boat, no depreciation deduction is allowed — but you may be eligible to write off the 50% of the costs of boat fuel, food and drinks, and even the fish bait, if you qualify under the usual business entertainment rules. More Tips Available These tips show that tax planning doesn’t have to be tedious. Whether you decide to ship the kids off to day camp or take the plunge of buying a boat, summer tax planning can actually be fun — and your tax advisor may have other creative ideas. With the proper planning, you can bask in the sun and tax-saving opportunities all summer long. The TMA Small Business Accounting, P.C. Their staff has been delivering professional services to small businesses in Central Indiana for over 20 years. Having worked with hundreds of small business clients, we have significant expertise with a wide variety of service businesses in Indiana. We have especially strong experience and expertise in working with businesses in the healthcare (medical, dental, etc.) and foodservice (restaurants, caterers, etc.)  Almost two years ago last month, Americans for Annuity Protection gave this speech at the United Nations Global Economic Summit. We were thrilled and awed by a dozen other speakers with their messages. They are as relevant today, if not more. Here was ours… Longevity is rapidly changing our nation and the world. We are at the midst of the global longevity revolution. A revolution that will have a bigger impact on society and culture than the industrial revolution and the technology revolution. It is something that has never occurred in human history. What is the impact on our nation and the world as the global birthrate drops and the life expectancies continue to extend? The remarkable 20th century breakthrough in medical sciences has given us a society that is living longer than ever before but now we don’t know how to finance longer life spans? Today in America, someone is retiring every nine seconds. That means, every nine seconds someone is applying for entitlement benefits. Can we afford it? Can we afford longevity? Are we prepared for an aging nation, and an aging world? How do we live longer lives that are better lives considering the rising healthcare costs, low interest rates, less from Social Security and increased taxation? Between this year and through 2030, the 65 plus population will grow by more than 70% while payroll taxes will grow by less than 10%. Where is the money going to come from? Between 1991 and 2007, bankruptcy filings have increased 125% for people between 65 and 74 and 400% for people over 75. The bottom-line is, millions won’t have enough money for the comfortable retirement our parents and Grandparents enjoyed. We are simply facing a national retirement crisis in America. Millions will find that they are too old to return to work and have too little in savings. Half of today’s private sector workers don’t have any employer sponsored retirement plan and over 2.5 Million Boomers have less than $1000 in their net lifetime of assets saved. The Great Recession saw a decline from pensions and savings of over five trillion. Today most have recovered but could we survive another economic catastrophe? Especially if millions are relying on a monthly income that’s got to last until their last breath. Americans need a lifetime income, free from the unpredictability of the turbulent storms of Wall Street. I’m an advocate for a solution, that I’ve made it my life’s work and is my passion to educate Americans about it. It’s the truth and remarkable magical use of Fixed Annuities. You see, based on the issues I’ve just discussed, Annuities make sure you don’t run out of money as long as you live no matter how long you live, AND they also make sure you don’t lose any money when the markets do. Annuities provided solid retirement confidence in an uncertain world and Annuities can make sure extra expenses like education, long term care and medical expenses are paid. You can even provide for an educational or additional income for your Children or Grandchildren. In a recent landmark article, which appeared in the Harvard Business Review called, “The Crisis in Retirement Planning”, by the recipient of the Nobel Prize in Economic Sciences. The author is a distinguished Professor of Finance at MIT. Dr. Robert Merton eloquently stated, “Our approach to saving is all wrong: We need to think about monthly income, not net worth”. He further states, “Investments cannot deliver security in terms of income”. If we don’t sound the alarm and educate consumers, the crisis will become a tragedy on a massive scale. Unfortunately one would think the Government would boldly embrace Fixed Annuities but instead the Department of Labor is attempting to damage the consumer’s ability to secure private commercial solution. The effect will be, increased costs, Government red tape, not consumer protection as it is disguised. This has led me and my colleagues to form a National Advocacy non-profit called, “Americans for Annuity Protection”. It’s a 501(c) based on the fact that Americans are in danger of losing a vital part of their financial heritage and liberty because of a lopsided campaign against Annuities and their market place, which have thrived and served the public nobly for centuries. The Longevity Revolution is in progress. The natural essential companion is the only vehicle that provides certainty, security, guarantees and a solid predictable income for life with market protection...the Fixed Annuity. Let’s not fail society when the solution is and has been successfully managing longevity risk for the last hundred years. Today annuity advisors strive to always put customers first. Addressing longevity risk is just one of the many risks they address and work to minimize or eliminate. Annuities provide an incontrovertible and unprecedented protection from longevity risk that no other financial product can achieve… guaranteed income that will last as long as you do. Americans for Annuity Protection is dedicated to securing AMERICANS prosperity through guaranteed insurance solutions using annuities. Ask a Safe Money Advisor for more information today!

I’ve been fortunate to do a lot of things in my financial services career. I’ve been involved in buying insurance companies both here and in Europe. I’ve had the opportunity of serving as president of the US insurers, and had marketing responsibilities for the Luxembourg and Bermuda companies. And, I was able to be involved in the excitement of taking the holding company public on Wall Street. Boy, what can beat that? Simple... being a life insurance agent (Boy could that statement clear out a room or empty a party). But, that’s the truth. Yes, I’ve had a financial planning firm and sold a lot of securities but nothing can do what a life insurance policy can do. A life insurance policy is guaranteed “Dream Completion.” Let’s explore… The life insurance policy assures that people can complete their dreams, regardless of premature death, hurricanes, stock market crashes or acts of terrorism. A piece of paper, a drop of ink, and a premium builds an estate and nest egg that we all want to accumulate. Think about it this way: if people are dependent upon us, shouldn’t we guarantee their security... even if we are not around? I am sure that you would agree with a resounding yes. But, maybe I am talking to the wrong crowd. Let’s see. I am confident that you have been very fortunate in your careers. Some of you reading this are retired and some still out there kicking butt. But, should you die tomorrow and the person dependent upon you lives for many more years, will your financial holdings be enough to guarantee that person the security that you wish for them? If the answer is no, then you should be happy to purchase an additional policy, pay the premium and guarantee that the dreams will be completed. Yes, it is magic. No other, I repeat, no other financial instrument will do what a life insurance policy will do. So, why is it that some people say that they don’t like life insurance? What they really mean is that they don’t like paying for life insurance, but they like what life insurance does. So, in closing, I would challenge you to have a life insurance review with a member of The Safe Money Places Agent Network and see if you feel comfortable with the amount that you own. We all still have dreams... regardless of our age. Don’t you want to ensure that they are completed? It’s real simple and you have the power to do it. Be a “dream dealer” today and complete those dreams with life insurance.

Summertime is nigh, so pack your bags for some safe travels to some great American spots.

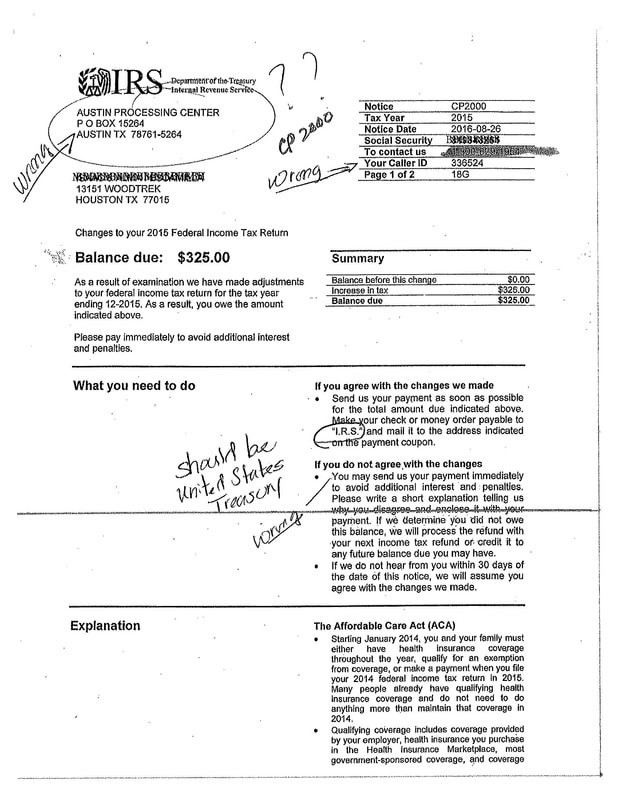

Such as Duluth. Yes, it’s slightly off the beaten path. But they have some wonderful parks, pleasant weather and maritime museums (it remains an active port). They have a passenger train that will haul you along the shoreline of Lake Superior. If you’re in the mood to walk, instead, you can hike to your heart’s content 310 miles from just south of town to the Canadian border along the Superior Hiking Trail. Be mindful of bears, even in town – last fall one spent an entire day climbing trees next to the downtown Radisson hotel. Staying with the Great Lakes theme, you can spend an entire summer alongside Lake Michigan in Milwaukee celebrating the many immigrant groups that have come to make up this city. Lakeside parks host fests for Poles, Mexicans, Germans, Scots, Italians, African Americans, etc. Conveniently filling in weekends when there is no migrant festival are a slew of beer fests in a city that is, after all, all about beer. Tired of lakeside beer and brats? Head into the lake itself, for fishing charters to chase down brown trout and salmon. License will be included with your charter fee. If you want to look down on water rather than splash about in it, try St. Louis and the St. Louis Gateway Arch, overlooking the Mississippi River from an observation deck open to one and all if you don’t mind riding 630 feet into the air in a tiny elevator. A westward glance from the Arch will show you the stadium for the storied Cardinals baseball team, always a fun way to spend an afternoon. Beyond that are two great, world-class attractions – a zoo that rivals San Diego and the Missouri Botanical Garden, which has been showing off flora and fauna since 1859. And there is some great food to be had in St. Louis – try “The Hill” neighborhood for down-home Italian fare. Busting out of the Midwest, check out Portland, Ore. Here, you can soak in vistas of the Cascade Mountains and Willamette and Columbia rivers astride a bicycle as the city is honeycombed with biking paths (ranging from blocks in length to 51 miles). There is a strong farm-to-table movement here, so you can easily indulge your locavore habits. At the end of the day – or earlier, why wait? - you can sip wine at one of the hundreds of wineries that dot the Willamette Valley, starting on the southern outskirts of town. Some of the country’s top pinot noir and pino gris come from here. You also can taste some decent local wines in Amarillo, Texas. Honest. They come from an area called the Llano Estacado, and could make for a perfect pairing to giant Texas T-bones they like to charbroil around here. Before dinner, check out the quirky Cadillac Ranch on the western edge of Amarillo – the one that showcases all those old huge-finned Cadillacs buried nose first into west Texas dirt. The Cadillac Ranch sits alongside the historic U.S. 66. In the city itself lies the U.S. Route 66-Sixth Street Historic District, now featuring no end of shops and old time filling stations to remind you of the early days of motoring. Speaking of motoring, drive south of town a bit to the Palo Duro Canyon State Park. There is a scenic highway that winds mile after mile through the second-largest canyon in the United States. Though not nearly as famed as Arizona’s Grand Canyon, here you can actually drive though it and in spots look upward 800 feet in spots. Over your own glass of wine, or beer or coffee, pull out an atlas and map out directions to one of these safe trips. Or let your fingers do the walking on the map and search out your own summertime destination. This article was written by: Steve Dinnen Mr. Dinnen served as Sr. Business Reporter for the Des Moines Register, Business News Editor for the Indianapolis Star and served as Editor (freelance) for the Christian Science Monitor of its weekly personal finance column  The IRS, taxpayers and tax preparers share a common enemy: identity thieves. We all have a part to play in the fight against tax-related identity theft. Your role starts by learning the mechanics and warning signs. From there, taxpayers can take proactive steps to protect their data online and at home.

Understand How Tax Fraud Happens Dishonest individuals may steal taxpayers’ personal and financial information from sources outside the IRS, such as social media accounts where people tend to share too many details or bogus phishing emails that appear to come from the IRS or a bank. Once they obtain an unsuspecting taxpayer’s data, thieves may use it to file fraudulent federal and state income tax returns, claiming significant refunds. Paperless e-filing facilitates these scams: Thieves submit returns electronically, based on falsified earnings, and receive refunds via mail or direct deposit. Sure, the IRS maintains records of wages and other types of taxable income reported by employers, but they don’t usually match these records to the information submitted electronically before issuing refund checks. By the time the IRS notifies a victim that it’s received another tax return in his or her name, the thief is long gone and has already cashed the refund check. In addition to refund fraud, thieves may use stolen personal information to access existing bank accounts and withdraw funds — or open new ones without the taxpayer’s knowledge. Criminals are becoming increasingly sophisticated and their ploys more complex, making identity theft harder to detect. Recognize the Warning Signs Taxpayers are the first line of defense against these scams. The IRS lists the following warning signs of tax-related identity theft: Your electronic tax return is rejected. When the IRS rejects your tax return, it could mean that someone else has filed a fraudulent return using your Social Security number. Before jumping to conclusions, first check that the information entered on the tax return is correct. Were any numbers transposed? Did your college-age dependent claim a personal exemption on his or her tax return? You’re asked to verify information on your tax return. The IRS holds suspicious tax returns and then sends letters to those taxpayers, asking them to verify certain information. This is especially likely to happen if you claim the Earned Income tax credit or the Additional Child tax credit, both of which have been targeted in refund frauds in previous tax years. If you didn’t file the tax return in question, it could mean that someone else has filed a fraudulent return using your Social Security number. You receive tax forms from an unknown employer. Watch out if you receive income information, such as a W-2 or 1099 form, from a company that you didn’t do work for in 2016. Someone else may be using the phony forms to claim a fraudulent refund. You receive a tax refund or transcript that you didn’t ask for. Identity thieves may test the validity of stolen personal information by sending paper refunds to your address, direct depositing refunds to your bank or requesting a transcript from the IRS. If these tests work, they may file a fraudulent return with your stolen data in the future. You receive a mysterious prepaid debit card. Identity thieves sometimes use your name and address to create an account for a reloadable prepaid debit card that they later use to collect a fraudulent electronic refund. If you suspect foul play, contact your tax preparer immediately. He or she can help determine whether you’re a victim of tax-related identity theft and identify steps to remedy the situation. Take Preventive Measures You may wonder how many taxpayers file electronic vs. paper returns. “There are 150 million households that file federal and state tax returns involving trillions of dollars…. More than 90% of these tax returns are prepared on a laptop, desktop or even a smartphone — whether they’re done by an individual or a tax preparer. This is a massive amount of sensitive data that identity thieves would love to get access to.… With 150 million households, someone right now is clicking on an email link they shouldn’t, or skipping an important computer security update, leaving them vulnerable to hackers,” said IRS Commissioner John Koskinen in a recent statement about the Security Summit Group. (See “IRS Creates Security Summit Group” above.) How can you actively safeguard your personal data online and at home? Here are four simple ways to thwart tax-related identity theft:

Another simple way to prevent someone from filing a fraudulent return is simply to file your return as soon as possible. The IRS begins processing tax returns on January 23. If you file a tax return before would-be fraudsters do, their refund claims are more likely to be rejected for filing under a duplicate Social Security number. Join the Fight The deadline for filing your 2016 return is fast approaching. The IRS expects more than 70% of taxpayers to receive a refund for 2016, and it’s on high alert for refund fraud and other tax-related identity theft schemes. You can help the IRS in its efforts to fight tax fraud by watching for these warning signs and safeguarding your personal and financial information. This article was written by: The TMA Small Business Accounting, P.C. Their staff has been delivering professional services to small businesses in Central Indiana for over 20 years. Having worked with hundreds of small business clients, we have significant expertise with a wide variety of service businesses in Indiana. We have especially strong experience and expertise in working with businesses in the healthcare (medical, dental, etc.) and foodservice (restaurants, caterers, etc.) industries.  It has been a privilege to have lived in this great United States for almost eighty-two years. In that time, I have considered it an honor and duty to have voted consistently for local, state, and national offices seekers for over sixty-one years. More importantly, I have had a direct responsibility in electing a number of significant office holders in campaigns for Mayors, Governors, Congressional Representatives, Senators, and Presidents. All of these men and women had one common denominator – LEADERSHIP!

What makes a leader a leader? There are any number of traits that added together provide leadership qualities. Finding these attributes in a person who aspires for political office, can be difficult to determine – primarily because it is in the eyes of the beholder as to what makes an outstanding candidate. Certainly the person aspiring to a particular office gives some strong indications as to his or her achievements and qualifications. Even so, we often approach a voting machine with a lack of knowledge as to the reasons for our selections. Our votes are often cast because it boils down to name recognition as to the person in whom we place our confidence. Leadership is a privilege which brings responsibilities. Strong leaders set goals and objectives and follow through with them. They listen, communicate well and lead by example. Selecting a team who work well together while being willing to take on challenges is vital. There was one civic leader who embodied all these qualities and more. William H. Hudnut III, demonstrated leadership qualities. He served as Mayor of Indianapolis for four terms – sixteen years – from 1976 – 1992. Born October 17,1932, during the Depression, he had a distinguished record of achievement over more than eighty-four years. He was Mayor of the Capital City of Indiana; Senior Pastor at Second Presbyterian Church from 1964 – 1972. In 1973, Hudnut answered the call to represent Indiana in the U.S. House of Representatives. However, it was in the capacity of Minister-Mayor that his “Leadership Qualities” blossomed and bore fruit. It has been stated that Bill Hudnut, “Built well and he cared about people.” If it were that simple, many people could have taken up the mantle of office and achieved success. No, I firmly believe that Mayor Bill brought so much more of his personal attributes to the office and embellished those which he inherited along the way. His vision transformed a city from a sleepy, stodgy, run-down entity into a vibrant, wide-awake and proud city. He has been called a “gutsy” Mayor. That means he took chances where few existed. However, Bill Hudnut was more than a risk taker. He was calculating in his choices, and weighed carefully the outcomes. He understood what it meant to “stick his neck out” because he built a lifetime of achievements based on doing what others did not expect. The results speak for themselves. He was famous for building a major-league stadium when Indianapolis didn’t have an NFL Team. He saved the Indiana Pacers NBA Basketball Team by enticing Herb and Melvin Simon to buy the franchise before it could be sold to a west coast city. He launched an effort to bring the Pan American Games to Indianapolis when other city mayors turned thumbs down because of a lack of time. The Games were a huge success because thousands of volunteers backed Hudnut’s challenge to make the Games a success. This single act brought recognition to Indy and sparked a resurgence in amateur and professional sports that is still being felt today. He believed in the city. More importantly, he believed in its people. Circle City Mall was another project that took roots and grew because he believed it was a needed element to preserve and build a vibrant downtown. The movement of business to the outskirts of the city had badly tarnished the center of Indianapolis. Hudnut called Circle City “the crown jewel” of his effort to revitalize the center of Indy. He formed a coalition of top local companies and personalities to get the job done. Hudnut was a man of humor. What other Mayors would dress-up as a 6 foot 5 inch leprechaun and dance through a whole parade? How about riding a snow plow during the middle of a terrible snow storm helping to clean the streets? Or, practicing the famous “Hudnut Hook Shot” hitting a trashcan with regularity to emphasize cleaning the city? Here was a man who didn’t always take himself seriously. His faith and experience as a minister paid dividends, as well. He knew how to motivate people and build consensus. He genuinely listened to people and was compassionate in his responses to their needs. He sought citizens with diverse backgrounds and from different cultures and then strengthened the bonds between them to form a cohesive culture. His love for the city, its people and his ability to listen to criticism and compromise when necessary brought Indianapolis out of a downward spiral and assured success where there had been little before. He was the first to admit that he had not accomplished success on his own. It took a teamwork philosophy, but there is always someone at the head of the parade – even in a green leprechaun suit to get the job done. Bill Hudnut passed away on December 18, 2016. His vision, leadership and heritage will continue to live on for many years to come.  Would you prefer your retirement income to:

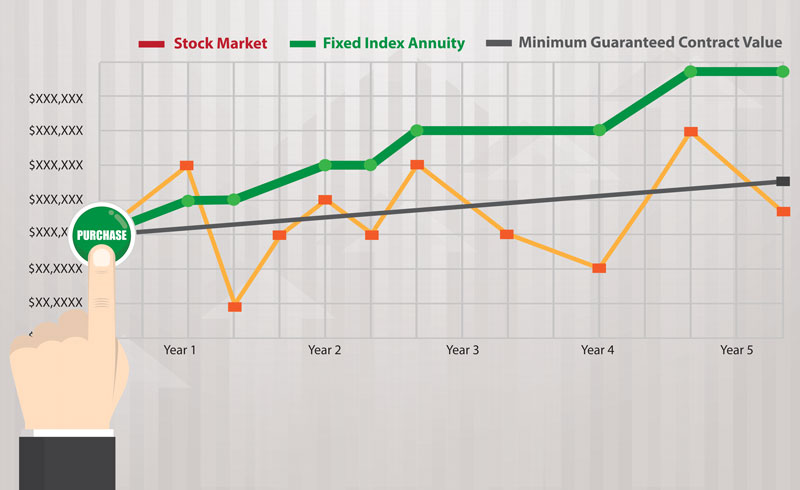

Wall Street financial writers try to frame retirement planning as creating a large enough pile of investments to last through retirement. This approach has merit if the retirement goal is to leave money to your heirs, but the typical main goal in retirement planning is to have enough income. Since Wall Street manufactures investments, their go-to solution to generating retirement income is to withdraw a percentage of your investments and hope it lasts. The problem is there are no guarantees with this withdrawal approach, so the suggested withdrawal percentage keeps getting lower. For years, the suggested “safe” withdrawal rate was 5%. This was generally reduced to 4% about two decades ago, but even at 4% the risk of running out of money early is as high as 32%*, so several advisors suggest that taking out 3% might be a better idea – or even limiting withdrawals to 2% from your investments each year would be prudent. The problem is most people saved for retirement with the expectation that the $500,000 they managed to put away would get them $25,000 a year and now they’re being told they should tighten their belt and settle for $10,000 in retirement income, to lessen the chance it becomes $0 down the road. The odds that you won’t run out of money – even when taking out 4% a year – are still on your side. Based on the computer simulations that Wall Streeters like to run, in most scenarios not only does your income not go down but it increases. However, the question that remains is how big of a gambler are you? The insurance world approaches retirement in a different way. Wall Street is all about managing the amount of risk the retiree retains; insurance companies transfer away the risk of income loss from the retiree to the insurer. They do this through an annuity in many different ways. Income choices from an annuity produce stable income that does not go down – even if the stock market or interest rates do – or can even automatically increase the income each year during retirement. The retiree can choose annuities where they have access to the cash value of the account and at least ensure that they (and any heirs) will get back all of what they put in. And these income choices guarantee that the income will last as long as the retiree does. These are the reasons that millions of retirees own annuities. This is not saying that a retiree should place all of their money in annuities, but it does mean one should look at their personal situation and determine how much stable income they desire and whether an annuity income choice might be prudent. * Finke, M. Pfau, W, & Blanchett, D. 2013, “The 4 Percent Rule Is Not Safe in a Low-Yield World,” Journal of Financial Planning, 26, 6: 46–55.

I was only a kid when a 16 ounce pound of coffee suddenly became 15 ounces, then 14, then 13, but other groceries stayed the same size for quite a while. It wasn’t until the mid ‘90s that some ice cream makers very quietly reduced the size of their half gallon to 1.75 quarts, since reduced to 1.5 quarts. After the millennium recession we witnessed several makers of bagged foods (cereals, chips, pretzels and such) reduce the quantity of the contents without reducing the size of the bag or the cost. The biggest kick in the shorts was what happened to toilet paper. It was bad enough that the paper on a roll shrunk from 468.7 square feet to 352 square feet – a 25% reduction in product size with no reduction in product price – but the TP makers tried to tell us this was better because they were now offering “double rolls” which is a meaningless marketing claim (I filed a complaint with the Federal Trade Commission about this false advertising, unfortunately the response back was “seriously?”, so I don’t think the Feds will be intervening in the TP scandal anytime soon).

However, the Feds did intervene in what I was earning on my savings. Back in 2007 the interest paid on my bank savings averaged 4.1%. As the Federal Reserve Board intervened the average CD rate rather quickly dropped to 2% by the end of 2008, it fell to 1% by the middle of 2009 and today the average one-year CD rate is 0.3%. CD interest income has shrunk by over 90% in 5 years. A fixed annuity can guarantee your income will increase in future years even if rates do not Every savings vehicle has been affected by yield shrinkage, but some offer more protection than others. Although current interest rates on fixed annuities have fallen just like other vehicles, fixed annuities guarantee that at least a minimum interest rate will always be earned, so money set aside to grow will continue to grow. If the goal is income, fixed annuities offer a couple of ways to receive an income that will never go down and can even go up. One of these is through an income annuity that provides a set income for a specific number of years – or even for life. Another option that is rapidly growing in use is a lifetime withdrawal benefit that guarantees a minimum annual income and access to the cash value of the annuity. You can even find annuities where the income is guaranteed to increase each year even if interest rates do not. I don’t think the era of shrinkage is over. When I went to the paint store last month the sign on top said “paint $15/gallon” but the paint can said it contained three and three quarter quarts. I wouldn’t be surprised if the way they eventually deal with the high price of gas is to say a gallon contain 3 quarts – and then brag about how the price is finally under $3 a “gallon”. However, in this steadily shrinking world there is one thing that won’t get smaller and that is the guarantee on your fixed annuity. This article was written by: Dr. Jack Marrion Dr. Marrion is the founder of SafeMoneyPlaces.com. His research on senior decision making and the financial world have been featured in hundreds of publications.  The Thanksgiving and Christmas Seasons in my household were always times of special occurrences. Family gatherings, traditions in the majority of households, took on very special meanings among our relatives both in the city and country.

The memories of these gatherings live on even though those who were associated with those times have passed away many years ago. As an urban family, we normally celebrated Thanksgiving on the Wednesday prior to the actual holiday on Thursday. The reason for this advanced dinner arrangement primarily was concerned with my father, a practicing physician, who was able to arrange his house calls to coincide with dinner plans that included his mother, father, sister and other members of his immediate family. These functions were always held at our home in Homecroft – just south of Indianapolis. My mother prepared a large meal with all the trimmings – including all the traditional goodies of turkey, oyster dressing, cranberries, sweet potatoes, green bean casserole and pumpkin pie. My Dad always insisted on mince meat pie for his dessert. From my memory, he only took one slice of the pie, and didn’t follow-up with it in the remaining part of the holiday. On Thanksgiving Day, we loaded the car and headed toward relatives homes in southern Indiana. My Mom was a country girl, and this part of the celebration was always held at one of her family members’ homes. These gatherings were traditionally large in nature with upwards of thirty plus adults and kids featuring food selections galore. There was always turkey, ham, chicken, wild game, a dozen or so salads and many, many desserts. Some of those delicacies came straight out of cast-iron stoves that used corn cobs or charcoal for fire. How these delicious goodies came to the table with such humble beginnings always amazed me. After emptying our plates and letting our stomachs digest all the wonderful treats, the activities would begin. Depending on the weather, the men would head to the cornfields to see if they could scare up a rabbit or two. The cousins would engage in a flag football game which would eventually end up in some form of roughshod tackle event. If the weather didn’t cooperate for an athletic endeavor, my uncles would play a cut-throat euchre game while the ladies retired to the kitchen to catch-up on family affairs. A major part of their discussion centered on drawing names for the Christmas gift giving. Because of family size, the amounts to be spent were always under ten dollars. However, more was spent on our grandparents. Christmas Eve followed suit with the celebration being held in the city. Once again, this holiday had many traditions. There were the days of sorting and checking decorations that were always a scrambled mess; addressing Christmas cards; decorating the inside and outside of the home and purchasing gifts for the family. The expectation ran high throughout the month of December until it reached a fever pitch on the 24th. My Dad always made house calls into the evening until my sister and I could hardly stand the suspense. When we were smaller, we were sure that Santa Claus would pass us by if we weren’t close by the tree. Obviously, that didn’t happen, but adult family members always insisted that we eat something before Santa could appear. That only added to the thrill when we were allowed to finally enter the living room where the toys would mysteriously appear before our “wondrous eyes!” On Christmas Day, we would trek south again for a day filled with households of people, food and gift giving. Keep in mind, these were the days before television, consequently we younger cousins had to amuse ourselves while awaiting for St. Nicholas to appear. He always seemed to come at about the same time, and his suit appeared as if he had spent a good portion of the year building the toys while wearing it. To this day, I can’t be sure which of the uncles took the key role of Santa’s helper in passing out the gifts. Each of the cousins received a two dollar gift from the grandparents. The adults were given five dollars. Then the various exchanges were made with everyone exclaiming, “How did you know that’s what I wanted?” To me, the saddest time of year was immediately following the Christmas Season. The expectations were over for the year. It would be months before the families would gather again. The cold weather would bluster and bury us in ice and snow, and the walks to school seemed much longer in the shorter days of daylight. As I grow older, the memories remain, yet I long for the times when the families gathered for the holidays. That doesn’t happen as frequently any more. Thanksgiving and Christmas are still celebrated, but with fewer and fewer people attending. I would relish a day filled with the joy and cheer of those long ago times. And, we wouldn’t turn on the television set! This article was written by: Norm Wilkens A nationally recognized speaker and writer, Norman Wilkens has traveled to forty-seven of the fifty states speaking on topics of marketing, advertising and public relations.  Tis better to give than receive. Tis likewise better to give wisely, to a charity or non-profit organization that you believe will safeguard your donation as it works to end hunger or poverty or protect animals and the planet.

A number of organizations look at the non-profit world to see who’s doing a good job of minding your money and spending it on relief efforts rather than executive salaries or fund raising. See the web references below for indexes that will summarize which large charities are doing the most with your money. A nifty guide published in the Christian Science Monitor shows that the nation’s largest charity, the YMCA, spends 87 percent of its expenses on programming. Charitywatch give it a grade of A. The YWCA, however, spends just 36 percent of its money on programming, and Charitywatch hands it a D-F grade. Sometimes a little investigating will help guide your decision. Let’s look at Goodwill Industries. Nationally, it’s one of the largest and most respected and gets high marks for spending most of its money on programs and not so much on its executive salary. But what about local Goodwills? Well, the Omaha World Herald just ran a series about the $900,000 salary and bonus paid to the CEO of Goodwill of Omaha (he also got a country club membership). More than a dozen Goodwill of Omaha executives – including the CEO’s daughter – earned more than $100,000 yearly. (The CEO has since resigned and a management shakeup is underway). The World Herald ferreted out much of its salary information from Form 990s. These are tax documents that most tax-exempt organizations must file every year with the IRS. They’re open for public inspection and you likely can look up a charity of your choosing from a database kept by Propublica.org. Two smart ways to give money are through your local United Way or community foundation. Both of these organizations should be expected to vett the charitable groups that they are supporting. Some of these community foundations tap into state or local income tax credit programs, so they can be especially appealing as a way to do good and help lower your tax bite beyond the regular deduction available for charitable donations. I prefer to give locally, and usually to support something I enjoy. I attend the local symphony, for instance, so I give them some money every year. I ride a bicycle a lot, and we have a good trail system where I live, so I support local biking groups. Some things have to be done on a bigger scale, however. If you want to help save elephants or gorillas, you have to go global. If you want to help provide medical care in war zones, then Doctors Without Borders deserves your check. And of course, there’s always your local church. If you’re attending there on a regular basis you already will know how your money is going to be spent. Here are web addresses for further study on charitable giving:  Article Highlights: