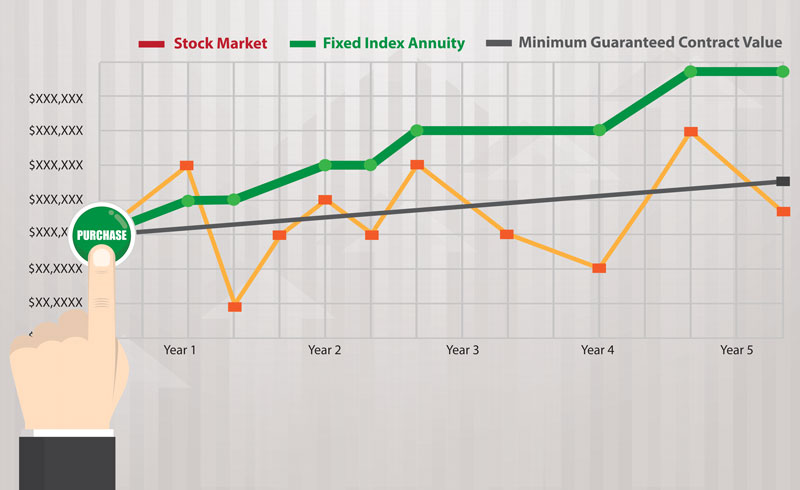

Actually my wife and I each bought one. The reasons we’d never purchased a fixed index annuity in the past were that we’re not particularly risk-averse and we had time to recover from any market downturn. The reason why we bought now was the recovery time-frame had shortened because retirement is looming. Although over the long-term the stock market has been a good bet, that isn’t always true when you’re looking at five or six year time spans. I was concerned we would need to start withdrawing from our investments before we recovered from the next bear market. We felt we needed guaranteed income to cover our expenses during retirement, so we created a retirement expense budget. The budget is, of course, an estimate, but we tried to include everything, added a bit more, and then added a bit on top for inflation. We then subtracted what the Social Security calculator says we’ll get in benefits and what was left was our guaranteed income gap. To fill the gap we purchased FIAs with guaranteed lifetime withdrawal benefits. I wanted the most certainty, so the one I chose had the most predictable joint lifetime income – and the highest annual fee. My main concern was money coming in each year, especially if I die first, and knowing the exact amount of that future check when I bought. My wife wanted a lower annuity lifetime benefit fee and the potential for more income, so the FIA she chose doesn’t have as strong a base income guarantee, but offers the potential for higher income than I’m getting if she earns more interest during the deferral period. Her guaranteed base income is little lower than mine, but she could wind up getting a higher lifetime income than me when she begins to take withdrawals. Might we get a higher income if we just left the money in the market? Sure, and that’s why a large portion of our assets continues to be in investments. If we want guaranteed income, why didn’t we just buy immediate annuities? With the FIAs we have access to the cash value. The odds are we’ll be taking out more than we earn, so the account value will go down, but we have control over the account. If we needed to we could cash in the annuity and take whatever is left. And, like a life immediate annuity, even when our money is gone the FIA annuity company keeps paying for as long as we live. Do I believe we would have run out of money early if we hadn’t bought the annuities? No. I’ve done the math. The reality is we’ll probably both be dead before our accounts go to zero. Then why did we buy? It comes down to peace of mind. I know the income my wife and I will get from the annuities and it doesn’t matter what the financial markets do. This is the one piece of our portfolio we don’t have to worry about (it’s also the part of the portfolio my widow won’t have to mess with). Finally, if our minds get foggier in the future this is again the one thing we don’t have to fuss with. The trigger that caused us to take action and buy the annuities was doing the budget and seeing the guaranteed income shortfall (as a side note, my annuity income is more than enough to cover our real estate taxes and homeowners insurance, so I feel like it is our “always have a home” annuity). Planning for retirement gets very real when you’re looking at the hard dollars you will need in a rapidly nearing future.

Illnesses and health conditions are the reasons many seniors take early retirement. Whether they are physical, like MS, or mentally crippling conditions like depression or Alzheimer’s, illnesses that manifest during old age can have a big impact on quality of life. For many, choosing to retire simply isn’t a financial option, but their health demands that they take leave from work. Let’s look at some things seniors should think about when considering to retire due to an illness.

Consider Options Whether suddenly impacted by an illness, or experiencing onset symptoms of an illness or medical condition over time, seniors forced out of the workforce by illness need options. Regardless of the situation, employers are legally required to make reasonable adjustments so that their employees with illnesses are accommodated. Further, FMLA provides those with certain illnesses the right to time off work without penalty. Many folks worry about whether or not they can practically stop working because of an illness. What’s important to remember is that there are many sources of retirement income that pad out a retiree’s retirement fund. It’s not all decided by the amount of retirement benefit you’ve built up in your retirement fund, but also considers Social Security Benefits as well as Medicaid and Medicare benefits as well. Still, there are a few other options to consider. Part Time Options Some choose to work a more flexible schedule—or even part-time—if possible. Retiring completely isn’t always feasible, especially if it’s because of a sudden, unplanned illness. Many folks develop a retirement plan without much room for deviations. In these cases, even a few years can make quite a difference in the retirement plan when it comes to building finances. Part-time employments can give those with an illness the opportunity to continue working and earning their respective retirement benefits while also allowing for necessary time off to recoup. If the illness allows, consider adopting a more flexible schedule or only taking part-time responsibilities. It’s important to keep in mind that your physical and mental health are the most important. Whether you’re able to comfortably work through your illness or not, it’s good practice to set limits and keep yourself at a practical work level. Sometimes part-time work is doable, but it’s not always practical. Consider your illness, the symptoms you experience, your finances, and whether or not continued work will have a negative impact on your overall health and illness. Of course, instead of basing your decision solely on the financial implications, consider all aspects of your wellness. Voluntary Redundancy In some cases, taking voluntary redundancy can be the right option for your quality of life. Voluntary redundancy is a financial incentive offered by an organization to current employees to voluntarily resign from their position. They are most common among times of company restructuring or downsizing; however, they may also be presented to seniors nearing retirement, especially those who are suffering with an illness and the work becomes difficult to perform. A clear advantage of taking redundancy is that it would come with redundancy pay, which might make the decision to retire early easier to make. Consider Finances Whether an illness is present or not, most working seniors are already thinking about retirement. In most cases, seniors must wait until they are at least 62 before they can start claiming their pension—but those retiring due to a medical illness or condition may be able to access it earlier. One downside to retiring and claiming your pension early is that it won’t have as much time to grow as it would if you worked longer. However, when health is at risk, most don’t have much of an option. Every pension has its own details and definitions, so it’s important that you work out exactly what your retirement funds will look like. Start this process by finding out what your pension provider’s rules are surrounding ill-health and taking your pension early. Find out how much the pension is worth and how much income your pension sum can buy. In many cases, ill-health allows the pension holder to get an increased income—known as an enhanced income. After you’ve reviewed your financial situation, it’s a good practice to create a retirement budget in order to make sure that your retirement funds and income will be sufficient in covering all costs. Of course, in the case of illness even the support of a pension and partial income might not be enough to cover expenses. Many seniors might not be aware that they have options available for them to increase their retirement funds. One option is selling a life insurance policy through a life settlement. This article was written by: Leo LaGrotte I would be happy to answer any questions you may have about this or any other life settlement topic. I can be reached at 888-849-0887 or llagrotte@lsa-llc.com.  We strive to write about safe things in this column, so when the 2016 election came to mind, the word safe almost headed for the exit. I say almost, because there are safe ways you can participate in the process and not get dragged - badly, anyway - through the mud that’s being slung around so freely this election cycle.

For starters, you can vote. You can go to the polls in November and make your choice known. And you certainly could/should have gone to the polls for primary elections held during the Spring in your state. In my case, the effort started in January when I participated for the first time ever in the much-ballyhooed Iowa Caucus. Though born and raised in Iowa, I left at a tender age and returned in the late 1990s and began working as a reporter at The Des Moines Register. That job precluded me from participating in politics. But I no longer work at the Register, so I am free to get involved in politics. On a mild evening in January, my wife, adult daughter, and I trekked to an elementary school near to our home that served as the caucus selection site for Democrats from several precincts. We and 300-plus other people sorted ourselves out by preference for a particular candidate. For Democrats it seemed pretty easy - Hillary Clinton, Bernie Sanders or Martin O’Malley. Republicans at that time had a vastly wider field of candidates. Yet, the Democratic caucus was way more raucous because of how candidates are picked. Republican caucus goers simply write in the name of their candidate, go home and let the party brass count up the votes. For Democrats, candidates had to reach what is called viability – 15 percent or more of whoever showed up at each caucus site, standing for their candidate. We got a brief speech for each candidate from a volunteer supporter who, honest, stood on a lunch table to make a push for their man or woman. Then party functionaries literally counted heads of those who mustered under signs for each candidate. (These caucuses are run by the parties, not the government, so they follow their own peculiar rules). O’Malley didn’t reach viability, so his backers decided to throw in their lot with Hillary. A little messy, perhaps. But to my way of thinking it was democracy in action. It was the first-in-the-nation preference poll, if you will, to start the (crazy long) process of winnowing out winners and losers. And it was a completely safe, responsible way for me to participate; in some small way helping to decide who will lead this nation. In the fall, I’ve volunteered to work at the county election office. It will be a non-partisan effort on my part to help get people registered, advise them of polling stations, etc. and it has nothing to do with their political affiliation. We all need to vote, right? It seems to me that is a pretty safe way to help keep our democracy up and running. This article was written by: Steve Dinnen Mr. Dinnen served as Sr. Business Reporter for the Des Moines Register, Business News Editor for the Indianapolis Star and served as Editor (freelance) for the Christian Science Monitor of its weekly personal finance column  Article Highlights:

It is not uncommon for individuals to loan money to relatives to help them buy a home. In those situations, it is also not uncommon for a loan to be undocumented or documented with an unsecured note, and the unintended result that the homebuyer can’t claim a tax deduction for the interest paid to their helpful relative. The tax code describes qualified residence interest as interest paid or accrued during the tax year on acquisition indebtedness or home equity indebtedness with respect to any qualified residence of the taxpayer. It also provides that the term “acquisition indebtedness” means any indebtedness that is incurred in acquiring, constructing, or substantially improving any qualified residence of the taxpayer, and is secured by such residence. There are also limits on the amount of debt and number of qualified residences that a taxpayer may have for purposes of claiming a home mortgage interest tax deduction, but those details are not covered in this article, which focuses on the requirement that the debt be secured. Secured debt means a debt that is on the security of any instrument (such as a mortgage, deed of trust, or land contract): This article was written by: The TMA Small Business Accounting, P.C. Their staff has been delivering professional services to small businesses in Central Indiana for over 20 years. Having worked with hundreds of small business clients, we have significant expertise with a wide variety of service businesses in Indiana. We have especially strong experience and expertise in working with businesses in the healthcare (medical, dental, etc.) and foodservice (restaurants, caterers, etc.) |