Let me state at the outset of this article, that “downsizing” is not for the faint of heart. After a little over eight decades of living; more than twenty-eight years of marriage; almost too many moves to remember and dozens of disarrayed storage closets, it is not only difficult to comprehend, it is just about impossible to fathom. I suppose it happens to the best of us at least once in our lives. We go along throughout our twenties and thirties accumulating boxes of memorabilia - momentous piles of significant keepsakes that we just can’t part with. Our forties and fifties don’t improve the storage picture, we just add to the junk pile hidden in secret places we alone are allowed to enter because no one else would dare to disturb our cache of treasures. The sixties and seventies should prove the worth of our valuables, but often there is only a little more dust on the faded folders and forgotten reasons why they were saved in the first place. You have the right to ask and know what type of memorabilia I saved over the years. Taking stock of the many treasures accumulated, I found materials covering years of ads and commercials for varied clients. There were archives honoring political campaigns for candidates of local, state and national level. There was a wealth of pictures from grade school, high school and college days along with grades that weren’t always so glorious. I found speeches covering every topic from welcoming new students to honoring recent graduates. Family and friends were captured in slides, photos and movies that would take hours to sort through. The phrase “pack rat” began to take on a new meaning where I was concerned and I knew something had to be done, or many of the items saved would disappear in a wisp of dust and mildew. Downsizing opens the doors to a lot of questions. Once the decision had been made that it was time for us to downsize, we had details to work out. Where were we moving? How much room would we have? This was a major concern of mine considering the amount of stuff I have stored away. I have a store house of a lifetime of memories – most documented in one way or another. Personally, what was I going to do with a lifetime of accumulation of stagnant junk – most of which, as mentioned, had been unopened for a long time? This all has a happy ending. We made a successful move to a lovely home in East Texas near children, grandchildren and great grandchildren, all of whom have gone out of their way to assure our continuing comfort. And, yes, I shipped the boxes of my unopened accumulation! I am passing along the inherent wisdom of this article so that those of you who may be thinking this “will never happen to me”, can start making adjustments now – before it’s too late. I am still trying to unpack and sort through the boxes that I just couldn’t live without, but hardly ever opened. The lesson learned is very simple. Don’t wait till until the moving van is at your front door and the movers are asking what you want to take with you. Start “downsizing” your significant piles of precious artifacts asap! Suggest you start today! If you don’t, your kids, family members or friends, will end up doing it for you. They won’t understand why you kept all that stuff anyway!

Studies have found that we tend to get more risk averse about financial matters as we get older, especially after we hit age 50. However, aging, in and of itself, accounts for 60% of the increased dislike of risk. The balance is due to life events. We all don’t look at financial risk the same way. Not surprisingly, the rich are more tolerant of risk than the poor, as are those with college degrees, and some people simply enjoy the rush of taking a risk. Even so the studies show what- ever group you fall into, you are more likely to become a bit more reticent about exposing yourself to loss as you get older. This was originally thought to be purely a chronological thing, but it turns out life choices and life shocks affect how we perceive risk.

Even though each has the same income net worth and health picture, the change in the household changes their risk tolerance. The study also found that the effect of these life shocks is greater on women than men. Agents need to go beyond the financial questions to truly understand what is in the best interests of the consumer. Banks, J., E. Bassali & I. Mammi. 2019. Changing Risk Preferences at Older Ages. University of Venice No. 01/WP/2019

According to a recent study by the AARP of almost 4,000 people over 45, 13% said they still work some in retirement. And why not? For many seniors, some work in retirement can offer significant benefits, from adding extra spending power in a fixed budget, to giving seniors something new and exciting to do with all their extra time. Maybe you have friends or family who would benefit from a new source of income, but don’t want anything to do with regular schedules or a boring office. Good news! There’s never been a better time than 2019 to find work in the gig economy. Here are five different jobs you can share with your senior friends and family that require nothing more than a smartphone app and a desire to get to work. With these companies, seniors can take on as little or as much work as they want, so they can enjoy the freedom of retirement while still earning. UBER AND LYFT: PUTTING YOUR CAR TO WORK Across the country, Uber and Lyft are changing the way people get from A to B. These ridesharing apps allow anyone with a smartphone to hail a ride from nearby drivers—and those drivers can make some serious income! In fact, studies have shown that seniors are flocking to these rideshare apps in droves to earn some extra money using the vehicles they already own. To get started, all you need is to download the driver app for your smartphone. You also need a 4-door vehicle, a valid driver’s license, car insurance, and a vehicle registration. Drivers for Uber and Lyft can make an average of $8.55 to $11.77 per hour (as of 2018).[1] WAG!: TAKING YOUR LOVE FOR DOGS PRO Do you know a senior who loves animals and staying active? Wag! might be just the app for them. By signing up as a dog walker for Wag!, you can choose to walk local dogs in your neighborhood whenever you’d like—for pay. Wag! also offers dog sitting services for seniors who are happy to share their home with a furry friend for a few hours. Specifically, Wag! requires their walkers to be physically able to walk for at least 20 minutes at a time. They also have an application process that involves a quiz on dog care and safety, as well as your knowledge of harnesses and collars. In other words, this is a great fit for anybody who loves dogs and has experience with them. POSTMATES: DELIVERING HOT MEALS There are many apps available in most cities around the U.S. that allow hungry people to order delivery from virtually any restaurant they can imagine. Postmates is unique in that, unlike many of the other apps, they don’t require their couriers to own a car. When you sign up to deliver for Postmates, you’ll have the opportunity to take as many delivery orders as you’d like, and you’ll be responsible for picking up orders from restaurants and delivering them to homes and offices. All you need to sign up is a smartphone and a visit to the Postmates website. A bike or car to get around is optional. On average, Postmates couriers can expect to make up to $25 per hour. HANDY: HOUSEKEEPING AND HANDYWORK Do you know any seniors who have a knack for cleaning house or keeping everything in working order? Handy offers the chance for anyone with experience in housecleaning or handiwork to put their skills to work at their chosen pace.Unlike some of the other apps on this list, Handy does require contractors to have some professional experience—so this is best for that retired contractor you know, or your client who cleaned on the side a few years back. For the right person, however, Handy makes it easy to find jobs and get paid. Once you sign up and start working, you bring your own supplies to the job. Then, when a job is completed, Handy takes payment from the customer and deposits it directly into your bank account. Professionals working through Handy can expect to make anywhere from $22 to $45 an hour on their own schedules. SHIPT AND INSTACART: GROCERY SHOPPING FOR CASH In a world of smartphones, there’s nothing you can’t have delivered right to your door—and that even includes your groceries! Apps like Shipt and Instacart offer convenience for busy people who need to keep their pantry stocked, and they also offer a flexible way to make extra money. Seniors who can lift 30 pounds or more, who have a car, and are excited by the prospect of keeping active walking the aisles of their local superstore can register to be a shopper and start earning money right away. Today’s digital shoppers can typically expect to make up to $10 to $20 per hour. Are your senior clients looking to increase their spending power in retirement? Side jobs aren’t their only resource! Did you know you can sell all or a portion of a life insurance policy, even term insurance? At Life Settlement Advisors, we help trusted advisors just like you to give their senior clients the opportunity to sell unwanted or unneeded life insurance policies for more than the cash surrender value. Learn more about how you can start offering your clients this powerful financial tool, and contact us today to learn how we can help! CaseStudy: Harold and Dorothy bought life insurance when they were young to protect their children’s futures. Now the kids are grown and have good jobs, their youngest is 49 years old and they no longer needed the coverage. Harold’s financial advisor informed him he could sell his unwanted life insurance policy for an immediate cash payment. Harold and Dorothy sold their life insurance policy and used the proceeds to pay off a few medical bills, take a vacation and supplement their retirement.

Yes, I said “KASH” and not cash. Of course we need cash when either in retirement, or planning for retirement. But, today I want to focus on an acronym I learned many years ago, in a management class. The two week course was through Main Event Management. The title of the course was “Model-Netics”. At the time, the thought was that our business, personal, spiritual and family life revolved around 151 models. The course is still around today, and the number of models has increased past the 151 models at that time. But, “KASH” has been a guiding principle for me. The “K” stands for knowledge. Let’s relate this to retirement planning. Basically, the more knowledge that you have about this topic, the better your attitude (the A in KASH) in dealing with your retirement income goals, challenges, etc. The “S” stands for Skills. The better your planning skills, the better your chances of having a happy retirement. Finally, the “H” stands for habits. So, in a summary, the better your Knowledge, the better your Attitude, the better your Skills and it all becomes a Habit. So, how can you get more KASH? Let’s look at some opportunities. If you are nearing retirement, take some time to learn about options and choices. There are many different sites available to you. One, is this website!. Please explore and browse around. You can also go to the social security site. I would also go to your employer and take a look at your 401K plan. And, I suggest meeting with a financial professional. Check our his/her website, look for credentials, etc. Then, arrange an introductory phone call and determine if you want to meet. You do need a plan, and most of us need some help. You should also take a “risk tolerance” test. You can find many of these online. Also, forget what your friends are doing. It is your retirement and not theirs. Also, take a look at the birth date on your drivers license. Do you have enough time to overcome losses? And, be realistic. Knowledge in everything is key. A good attitude when planning is paramount. You still have time to improve your retirement planning skills. And, you need to make it a habit to give you the best shot at a happy retirement. Finally, there is always a time to start playing it safe. Are you more motivated by the hope for a huge gain, or the fear of a huge loss? That could give you direction. Stay safe my friends.

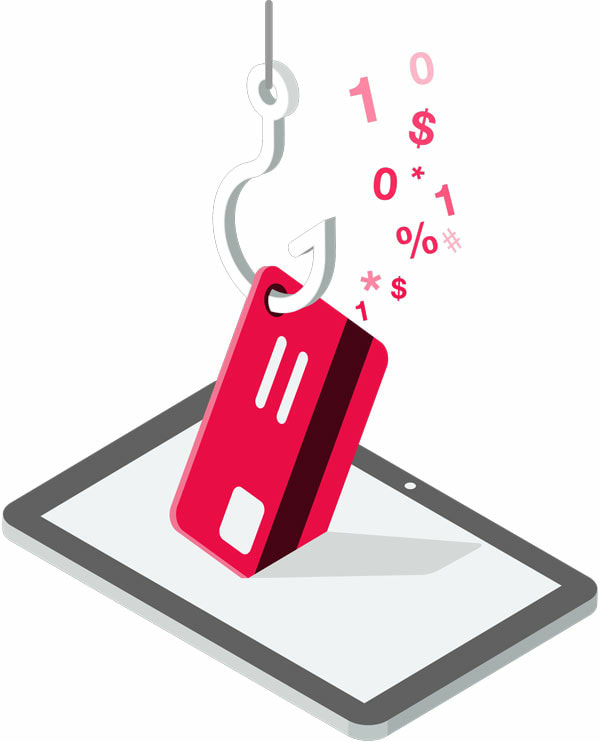

Chip Cards How do chip cards help fight payment card fraud? Chip cards — also known as Europay, MasterCard and Visa (EMV) cards — contain tiny metallic squares that are actually minicomputers, designed to generate a unique encrypted code for each transaction. Instead of being swiped, EMV-equipped cards are dipped into the merchant’s card reader for about 10 seconds, giving the card’s chip and the merchant’s terminal time to communicate. The time it takes to complete a chip-card transaction is similar to the time it takes to pay cash and receive change. Outside of the United States, chip cards typically require a personal identification number (PIN) to authenticate transactions. This enhances the security of chip cards issued abroad, because criminals must steal a payment card number along with the cardholder’s PIN. Many U.S. merchants have been reluctant to switch to chip-and-PIN cards, because some chip card readers aren’t equipped to accept PINs, just signatures. In addition, some cardholders aren’t in favor of memorizing PINs and, instead, prefer to authenticate transactions with signatures as they’ve done in the past. Magnetic Strip Cards By comparison, magnetic strip cards store static information, similar to old-fashioned music cassette tapes. Instead of dipping the payment card in a reader, cardholders swipe the card to allow the merchant’s POS to read the information encoded on the card’s magnetic strip. This outdated technology makes them easy targets for hackers. When issuing new chip-enabled cards, U.S. card issuers didn’t remove magnetic strips from the back of the new cards. While that decision provided merchants and their customers with two ways to complete transactions — and a backup in case a POS device was unable to read a chip — it reduced the pressure on merchants to invest in new POS chip readers. As a result, some merchants haven’t yet updated their card readers. When a cardholder swipes the magnetic strip on a chip card, instead of dipping it, they make it possible for criminals to steal data from the less secure magnetic strip. Once the information is stolen, it can be used to create a cloned card that can be used online or at merchants that haven’t upgraded their POS devices. Facilitating Secure Payments Consumers aren’t directly affected by the liability shift when their credit cards are dipped, instead of swiped. The change just transferred liability from credit card companies to merchants that continue to accept magnetic strip cards for in-store purchases. Consumers do, however, benefit indirectly from the shift, because chip cards generally offer a more secure payment method. Nonetheless, if criminals continue to steal U.S. payment card numbers from POS systems, cardholders still may be forced to accept replacement cards and then update their monthly autopayments for their new card numbers. This inconvenience, in turn, may cause consumers to pressure merchants to speed up their adoption of chip technology — and credit card companies to adopt PIN-and-chip technology. Merchants that haven’t yet upgraded their equipment and internal processing systems to allow for the processing of chip cards should do so immediately. In addition, they might consider enabling mobile near field communication (NFC) payments, such as Apple Pay or Google Wallet. Doing so is likely to minimize the long-term cost and hassle of upgrading card readers, as well as providing optimal flexibility and fraud protection when processing transactions for years to come.

And there were no waves to pound on me as I splashed about. We had been to Baja California the year before and found it, well, dangerous. That’s mainly due to its waves, which were 3-4 feet high when they hit the beach and could easily knock you down. We’d also been to the French Riviera, which is pretty but whose beaches are mostly rounded stones that are very uncomfortable to walk or lay on. Plus, partygoers in Nice sometimes haul in bottles and leave behind them, or their shards. If you want sand, try up the coast in Antibes. So that’s how I define a safe beach: Smooth sand coupled with placid, shallow waters that coddle even novices. Ideally there would be a lifeguard, though I saw none at Eagle Beach. The Red Cross has tips about safe swimming, including instructions on handling a rip tide. Check them out at: https://www.redcross.org/get-help/how-to-prepare-for-emergencies/types-of-emergencies/water-safety/beach-safety.html

|